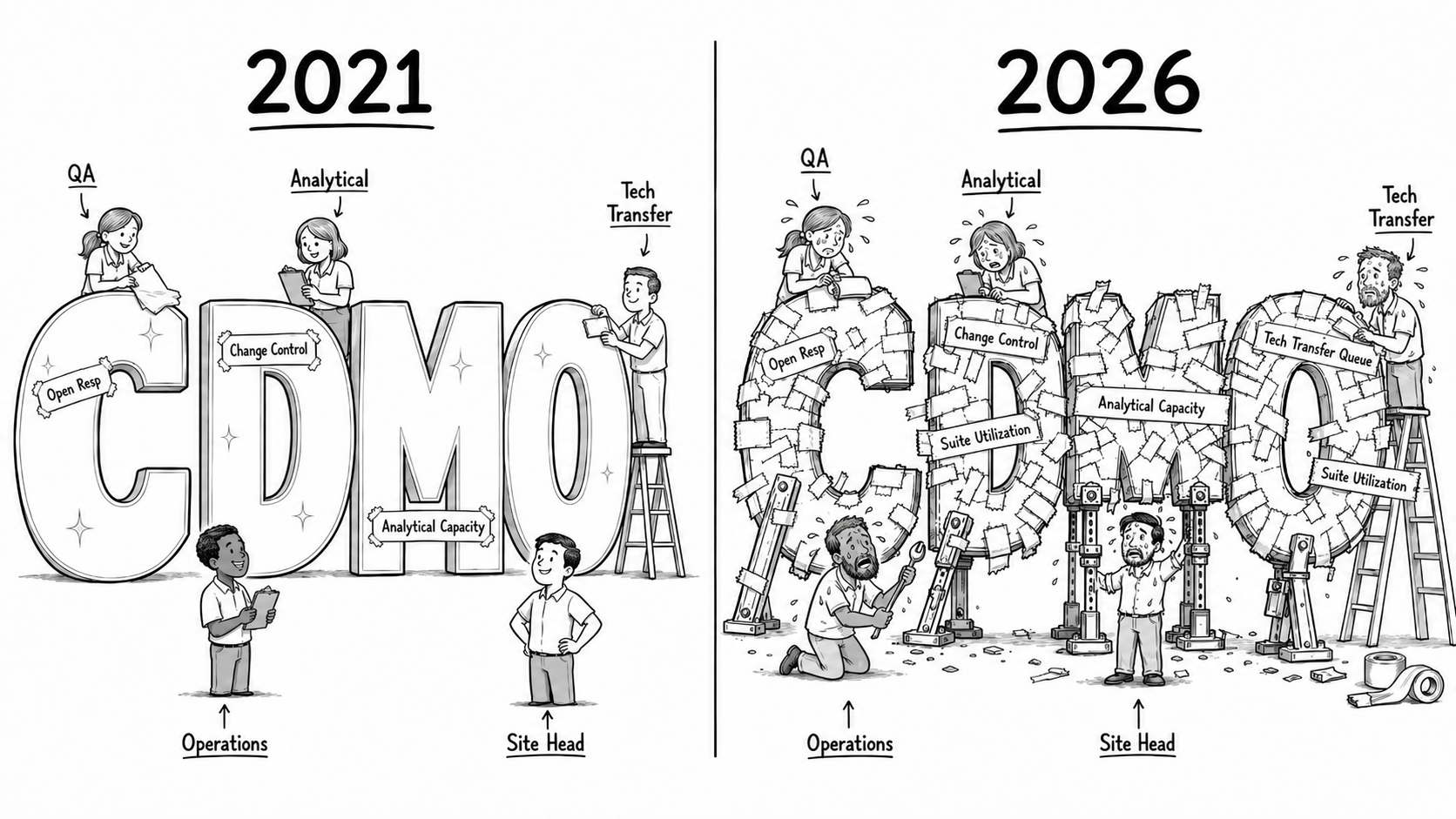

TL;DR: William Blair’s 2024 analysis: 85% of small biopharma outsource API, 77% outsource finished dose. The CDMO that once ran ten clients with four programs each is now running forty clients with one program each. Same total program count. Four times the tech transfer methodologies, analytical variability, testing protocols, and change control chains. (The four-times figure is an illustration of the complexity shift, not a measured count of clients per site.) The traditional CDMO operating model assumed economies of repetition. The reality is diseconomies of fragmentation, and the people on the floor are absorbing it.

This is part one of a five-part series on the CDMO industry: the strain it is carrying, the people inside it, and the choices the next decade will be built around. Part two covers what the headline numbers miss and the diligence questions biotech clients should be asking. Part three covers the pre-commercial to commercial inflection that catches small CDMOs by surprise. Part four covers what the CDMO leadership job actually develops. Part five covers why large brand CDMOs face a different version of the same problem.

If you work in CDMO sales, operations, or quality leadership, the last two to three years have been a grind. Not the missed-the-quarter kind. The other kind. Programs canceled at the client end before tech transfer is complete. Six-month RFPs that finish on the lowest credible price after the client promised price was not the deciding factor. Inspections arriving at a site managing a four-times explosion in change controls with the same headcount it had in 2021. Quality leaders working weekends to clear backlogs the operating model was never designed to absorb.

This experience is real. The people living it are not the reason the model is straining. They are the reason it is still standing.

After a decade of placing CDMO leadership and sitting in their planning conversations, this is an attempt to describe what so many of those leaders are managing, why the model has struggled to keep working, and what the conversation has to look like for it to repair.

Every biotech executive who has ever issued an RFP to a CDMO has written some version of the same wish list. The best team. The most flexibility. Consistency of execution. The highest quality standard. Deep GMP experience. No staff churn.

These are the right things to want, and every CDMO sales leader spends meaningful time demonstrating them in capability presentations, reference calls, and site visits. The list is so universally accepted that it has stopped functioning as a selection criterion. This list is the floor.

Which means the contract is won elsewhere. I see smaller CDMOs winning by being able to justify a defensible price against the program’s economics, by being the team that signals the most willingness to design around the client’s preferences rather than platform, and by being the team that accommodates most during the sales cycle: transparency of data, project management that gives proactive client attention. Price is a finalist filter. Accommodation is what gets you on the shortlist.

There is also a third list that does not get spoken about enough. The disqualification list. Modality experience. Regulatory history at the receiving site. Prior tech transfer outcomes with the client’s team if they have worked together before. The site head’s reputation. The CDMO team’s reputation among QA peers in the industry. It is a measure of reputation built on historic results, failures, and relationships.

In my experience, most senior CMC leaders, including CTOs and Heads of Quality, maintain this list informally. It is what gets a CDMO eliminated before the negotiation begins. Commercial leaders know it exists. The difficult part for any CDMO that has slipped onto the third list is resetting the trust bar by proving that the operation has actually changed.

So here is the rub. The first list describes a strategic capability. The second describes a transactional service. The third describes a reputation. The contract is signed against all three simultaneously, but the second is where so many CDMOs are feeling the pain, and where survival is decided. The irony is that the sales team is usually the first to be blamed.

Survival is not purely a sales-team failure. Buyers are sending signals that directly compete with profitability. But CDMO CEOs and boards own the commercial discipline that lets a sales team turn down a program, and they own the operational performance that lets the team deliver on the ones it signs.

A CDMO is a manufacturing business. The economics depend on three things:

The CDMO that achieves all three earns a return. A CDMO that achieves none cannot survive. Most operate somewhere in the middle, fighting for the third while losing ground on the first two.

Platformability sits at one end of a spectrum. Customization, attention, and accommodation sit at the other. The sales cycle sells the second. The operating model needs the first. Every CDMO leader I work with knows this. Most clients still expect both ends to be available at once. In years past that tension was manageable. From the third quarter of 2022, the math inverted.

Companies stripped pipelines. Discovery paused, Phase II narrowed to one or two programs, crossovers gone, Series B compressed. The mandate from boards was uniform: conserve cash, advance the lead asset, defer everything else. For the CDMOs serving those companies, the consequence was structural rather than cyclical.

Take a site with capacity for forty programs. In 2021, it likely ran ten clients with four programs each. One client’s analytical method covered four programs. One client’s tech transfer SOP covered four. One client’s change control regime covered four. The operating substrate had high reuse, and QA bandwidth matched a manageable number of program owners.

By 2024 and into 2026, that same site is far more likely to be running forty clients with one program each. Total program count is identical. Total complexity is not. Four times the tech transfer methodologies, each with its own bridging requirement. Four times the analytical method variability: different reference standards, columns, calibration regimes, acceptance criteria. Four times the testing protocols, change control approval chains, and SOP variants for the same unit operation. Four times the supplier qualification packages, audit cadences, and filing styles to support.

The volume in the suites is unchanged. The volume in QA, analytical, tech transfer, and the floor supervisor’s day is multiplied. Headcount has not scaled four to one. It cannot. The labor market does not support it (senior QA, validation, and analytical leads have run at elevated vacancy rates across the industry for two years), and the unit economics do not allow it. So the existing teams absorb the multiple.

The regulatory record is consistent with that strain. The FDA’s CRL repository, now more than 200 letters and growing, shows a Jefferies analysis (reported by BioSpace) finding more than half cite manufacturing and 41% cite product quality, and FDA-supported data compiled in the CTO Mandate Framework put contract and CDMO sites at roughly half of biologics facility-deficiency findings. Separately, the GAO reported that around 2,000 US drug plants, close to 42% of the registered base, were overdue for surveillance inspection after COVID. None of that proves fragmentation causes CRLs; a Head of Quality would not sign that chain without controlling for confounders. Read it as association: the visible consequence of a service model running on a fragmentation multiple that no operator chose and no client created on purpose.

The strain lands on three sets of shoulders, and the series is written with all three in the room. The CDMO executive is absorbing the fragmentation multiple and owns the commercial discipline that could relieve it. The biotech CEO and CTO are choosing a manufacturing partner whose capacity math now decides their program timeline as much as their own science does. And the Head of Talent placing CDMO leadership (the site heads, the QA and tech-transfer leaders holding the line) is hiring against a job that has quietly become far harder than its title suggests. The series is not written to defend the CDMO; it is written to make the choices legible to the people who sign the contracts and the people who staff them.

The four-times fragmentation is the visible number. The structural inputs underneath are where the conversation actually has to happen: modality differences, capital structure pressure, the BIOSECURE-driven geographic concentration, the forecasting moves large CDMOs have built into their books that smaller ones cannot, and what biotech clients should be doing about it before they sign their next contract. That is the work of part two.

Part two takes up what the CDMO headline numbers miss: modality, capital, geography, the client-drop oversubscription move, and the diligence questions biotech CMC leaders should be asking before they sign.

Every engagement begins with a diagnostic — a structured read on the role and the company you are actually inheriting.

Start a diagnostic