TL;DR: Across the 517 biotech equity investors with at least five portfolio companies, 90% follow on in fewer than half of what they back. Only 51 firms — about one in ten — re-invest in 50% or more. The median follow-on rate across the whole universe is 25%. The finding that surprised us most: this conviction has almost no predictive power for exit rate, with pooled exits across the three tiers landing at 37%, 34%, and 39% — the highest of the three belonging to the single-round tier. Read on for what that decoupling means when you are deciding whose check to take.

“We got the term sheet.”

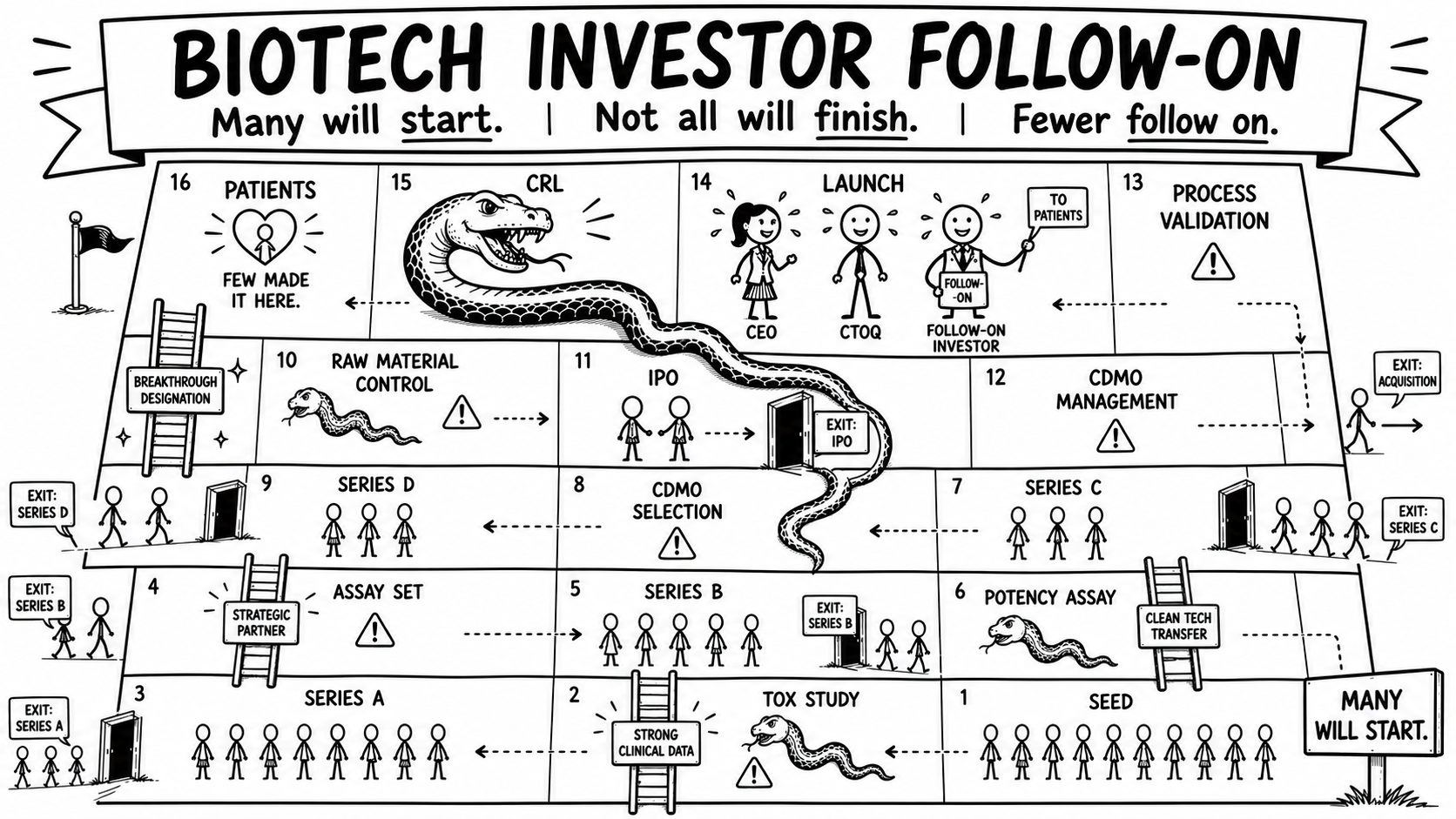

Every founder remembers the relief in that sentence. The round is the milestone the whole company has been pointed at for months, and closing it feels like the hard part is finally behind you. What the term sheet does not tell you is the thing that matters most over the next four years. It is whether the name at the bottom of it will still be there at the next round, and the one after that, once the work stops being a story you tell and becomes a tech transfer you have to execute.

To get at that, we pulled 30,486 verified biotech venture deal events from 2015 to 2026 and sorted every investor by a single number. Follow-on rate. Follow-on rate is the share of a firm’s portfolio companies in which it shows up again for a second round or more, and it says something a pitch never will. It tells you what kind of money you are taking on.

A closed round feels like validation, and in a real sense it is one. Someone with capital looked at your science and said yes. It is also the lowest-commitment moment in the whole relationship. Writing the first check is the easy part for an investor whose portfolio is built to spread those first checks widely and see what moves.

What separates one investor from another is everything that happens after that yes. When the data reads out soft, when the timeline slips, when the CDMO relationship has to change and the next raise gets harder — that is when you find out what the money was really for. Some firms lean in and lead the round that follows. Most quietly do not.

The Biotech Capital Report sorts the universe into three tiers by that behavior. Tier 1 is 51 firms that re-invest in half or more of their portfolio, at a median follow-on rate of 57%. These are the long-haul participants. Tier 2 is 162 firms that re-up more selectively, somewhere between one in three and one in two companies, at a median of 36%. Tier 3 is the largest group by some distance — 304 firms — re-investing in fewer than three of every ten companies at a median rate of 15%. In practice that bottom tier is single-round capital: one check, then gone.

Stand back and the shape is stark. The single-round tier holds 304 of the 517 firms, while the long-haul tier holds 51. For every investor whose record says it tends to stay, roughly six say it tends to leave. The median firm in the whole dataset re-ups in just one of every four of its companies.

This is where the easy reading falls apart. You would expect the firms that follow on the most to also produce the most exits. They do not. Pooled exit rates — the share of portfolio companies eventually acquired or taken public — come in at 37% for Tier 1, 34% for Tier 2, and 39% for Tier 3. The single-round tier posts the highest exit rate of the three. The conviction that looks so much like belief does not translate into more exits per company.

That reads like a paradox until you see the structure underneath it. Tier 3 is full of crossover funds, hedge funds, asset managers, public-market vehicles, and late-stage PE, and none of them are better pickers than anyone else. They enter at or near the exit by design, picking companies already tracking toward liquidity, so their high exit rate reflects when they arrive, not how well they choose. Tier 1 firms, by contrast, hold across the entire lifecycle, including the companies that quietly fail.

So the two numbers measure different things. Follow-on rate measures conviction over time; exit rate measures outcome at the company level. The report puts the implication in one line worth keeping: the structural difference is what you take their check for, not whether you take it.

The tier averages are useful, but they hide the more interesting detail. Once you look at individual firms, a few patterns sharpen the picture.

The starkest pattern sits inside pharma itself. A company’s venture arm often behaves nothing like its business development desk. SR One re-invests at 51%, which puts it in Tier 1 alongside the dedicated venture funds. Illumina Ventures at 48% and MRL Ventures Fund at 31% sit in Tier 2. Direct corporate activity from Merck, AbbVie, Sanofi, and others runs materially lower, because a BD desk is buying strategic optionality rather than making a multi-round financial commitment. It is the same logo on very different money. Which part of a company you are talking to tells you more than the brand on the door.

A related pattern shows up at the very bottom. Fourteen firms with ten or more portfolio companies recorded a 0% follow-on rate across the entire eleven-year window. The report withholds the names pending independent verification, which is the right call, but the structural commonality is plain. They span asset managers, crossover funds, healthcare systems, government and non-profit vehicles, and several pharma corporate venture arms. What they share is not a sector. It is single-shot capital by mandate. If one of them leads your round, you are taking on a specific kind of money, and the sensible move is to plan the next raise as if they will not be in it.

A third pattern is mostly mathematical: portfolio breadth and follow-on rate pull against each other. The widest portfolios in the dataset all sit outside Tier 1. RA Capital Management follows on at 30% across 188 companies, OrbiMed at 46% across 139, and Cormorant at 27% across 111. The largest Tier 1 books — ARCH at 109 companies and Atlas at 66 — sit right at the tier boundary. The widest nets are the hardest to keep re-casting, because the law of large numbers caps how high the percentage can climb. A broad-portfolio firm at 35% may show more absolute conviction than a narrow firm at 60%, so read the rate alongside the portfolio size, not on its own.

The last pattern is about stage, and it is the one a founder can act on directly, because firms concentrate where they are comfortable. SOSV dominates Seed with 124 participations. ARCH leads Series A at 90, with OrbiMed and RA Capital just behind. By Series B the order flips: RA Capital becomes the most active firm at 93, and it stays heaviest through Series C and D. Deerfield, by contrast, shows up mostly at Series C. Lay that map against your own timeline. If your hardest technical work lands at Series B but your investor concentrates at Seed and rarely follows on, they are the wrong partner for the stage where you will most need one.

All of this becomes a Phase 3 question the moment you ask why follow-on behavior matters so much in biotech specifically. The value-creating work in this industry is back-loaded and technical. The science earns the first check. What earns an approval is everything that comes after: making the process reproducible, transferring it to a commercial site, qualifying and then validating the analytical methods, surviving the first pre-approval inspection, and holding comparability together when the process has to change. None of that happens in the round you just closed. It happens in the long stretches between rounds.

Those stretches are exactly when single-round capital has already moved on. The crossover fund that came in late was never going to live through your tech transfer. The investor who priced your science at Series A but skipped the B was never pricing your manufacturing at all. The firms still on the cap table when the hard technical work surfaces are, disproportionately, the long-haul ones. They are the investors who sit through a CRL conversation, fund the redundancy a fragile supply chain needs, and back a CTO hire whose value will not show up in next quarter’s data.

One caveat belongs here, stated plainly. The dataset measures venture behavior, not regulatory or operational outcomes, so it does not prove that long-haul investors produce better CMC results. What it shows is who is structurally present when those results get made. The report also runs an eleven-year window on purpose, because follow-on is a slow-burning signal and a shorter lens would undercount the firms that come back. For a founder, that presence matters, because the investor who re-ups has incentives tied to your execution over years, not to a single markup.

You cannot change the structure of the capital markets, but you can be clear-eyed about which part of it you invite onto your cap table. Before you take the check, read the firm’s pattern rather than its pitch. Pull their portfolio and see how often they led or joined a second round. Ask the founders they have backed what happened when a program slipped, not when it soared. A handful of questions tend to separate the long-haul money from the tourists:

The aim is not to chase only Tier 1 names, since single-round capital has its place, especially close to an exit. The aim is to match the kind of money to the work in front of you. If the heaviest lifting still lies ahead — the CMC build, the tech transfer, the inspection readiness — bring on investors whose record says they stay for that part rather than leave before it begins.

There is a second use for this once an investor is on your board. Knowing whether a firm is long-haul or single-round tells you how to frame the technical case you bring into the room. A long-haul investor is underwriting execution across rounds, so a request to fund comparability work or a second source of supply lands as protecting the value they are compounding. A single-round investor watching the next markup hears the same request differently, and the argument has to connect to the milestone directly ahead and the strength of the coming raise. The CMC reality does not change. The way you make it land does. The CTO who can read the capital in the room is the one whose technical risks reach the board early enough to be acted on.

The same instinct runs through our CTO Mandate Framework, where boards and investors tend to judge biotech leaders on the science that opened the door, even though the value is created by the technical execution that comes much later. The Capital Report is the investor-side mirror of that idea. Most capital prices the science and moves on. The capital that compounds is the capital that stays for the part that is hard to do and easy to underestimate.

So when the term sheet finally comes, enjoy it. Then ask the quieter question sitting underneath it. Not how much, and not at what valuation, but who will be in the room two rounds from now, when the work that decides whether a medicine reaches a patient is finally on the table. The data says most of them will not be. The ones who will are worth knowing before you sign.

Source: The Biotech Capital Report 2026, Phase 3 Search — 30,486 verified deal events, 517 investors, 2015–2026.

Every engagement begins with a diagnostic — a structured read on the role and the company you are actually inheriting.

Start a diagnostic